Department for Communities and Local Government

Department for Work & Pensions

Funding of Supported Housing

Consultation response from The Riverside Group Ltd (Riverside)

- Introduction and background

1.1 The Riverside Group Ltd (referred to as Riverside) is one of the largest charitable housing association groups in the country, owning and managing over 53,000 homes. Riverside has a strong supported housing business, and each year our Care and Support Division delivers 300 services across 90 Local Authorities in England, serving approximately 5,000 older people and 3,600 individuals and families with a range of support needs[1]. In addition a number of other agencies deliver support to around 1,200 tenants living in Riverside owned homes. Our largest working age client group is the single homeless.

1.2 The provision of housing support to some of the country’s most vulnerable households is central to our mission. However given public sector funding cuts and impending rent reductions, the viability of many services has become marginal. Our supported and sheltered housing operations already run at an operating margin which is 17% lower than our general needs business, and we estimate that the proposed three year rent reduction will reduce our income by £4.3m per annum in perpetuity, or 11%, compared to original expectations. More than one in five of our supported housing schemes will become loss making following the rent reduction and we will be carefully reviewing our services as contracts come up for renewal.

1.3 There is much to welcome about the Secretary of State’s November 2016 announcement about the future funding of supported housing, not least the recognition of the importance of the sector and the broad commitment to maintain Government funding at current levels. We are pleased that this commitment has been reiterated in the recently published White Paper, ‘Fixing our Broken Housing Market’.

1.4 However we have fundamental misgivings about some of the details of the proposals, and believe that if these are not addressed, the very future of significant parts of the sector will be under threat, particularly given the challenging financial context we already face. This could be the final straw for many schemes and services. We see this as a once in a generation opportunity to ‘get this right’ and put supported housing on a sustainable footing.

- The financial impact of the Government’s proposal

2.1 On the eve of the proposed changes in April 2019, we forecast that Riverside tenants living in supported and sheltered housing will receive approximately £53m of housing benefit per annum. We have undertaken detailed analysis of what will happen to this income once LHA caps are applied, building a model taking individual rent and service charges in 2019 and comparing them to the LHA rates applicable in the locality by property size. We are then able to identify the extent to which the core rent and eligible service charge exceeds the LHA cap (if at all) for each individual tenancy and aggregate this up to local, regional and national levels – in other words the extent to which tenants will be required to depend upon local ‘top-up’ funding to meet their basic housing expenses[2]. We have run the model for Riverside alone, and for a group of five associations who have shared rent and service charge data[3].

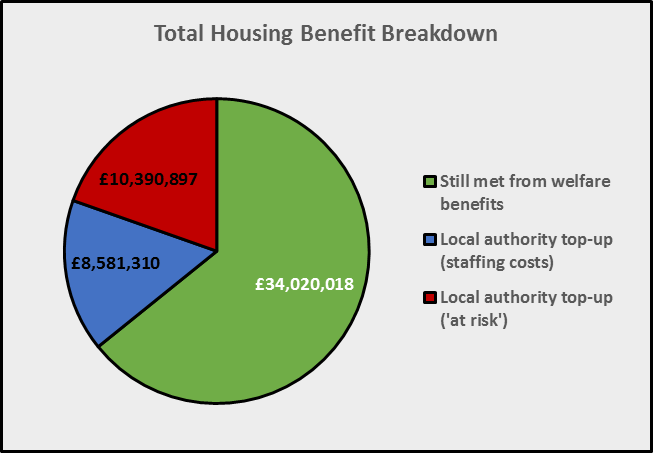

2.2 Figure 1 shows the high level output of the model for Riverside tenants, splitting current housing benefit income (adjusted to April 2019) into three components:

- Income which will still be met through benefits (capped to LHA rates) – green

- Rent and accommodation based service costs to be met through local top-up funds – red.

- Income for housing support (staffing) to be met through local top-up funds – blue

2.3 In total, over a third (36%) of support for tenants’ income will move from the entitlement based benefits system, to the local ‘top-up’ funding system. Over half of this is income which meets core rents and accommodation based service charges – £10.4m per annum – with the remainder meeting staff based housing support costs. We consider the former to be income which is ‘at risk’.

Figure 1: Riverside – breakdown of housing benefit income

Differences between supported and sheltered housing

2.4 Our analysis shows that two thirds of our tenants (who receive housing benefit) will have their benefit capped at LHA levels, proportionately more in sheltered housing than supported housing (table 2). There is a more marked difference in the scale of the capping effect, with weekly rents/service charges exceeding the caps by an average of over £65pw for supported housing tenants, representing over a fifth of total rent and accommodation based service charge income for tenants in receipt of housing benefit across all tenancies, in contrast to £26pw for sheltered tenants, or 16% of all income. This difference is primarily driven by particularly high accommodation based service charges in supported housing, given the highly specialised nature of the buildings and facilities management services required.

Table 2: The impact of LHA caps – Riverside

2.5 A very similar pattern plays out for the larger group of associations, with 25% of rent/service charge income being at risk for supported housing and 15% for sheltered housing.

Geographical Differences

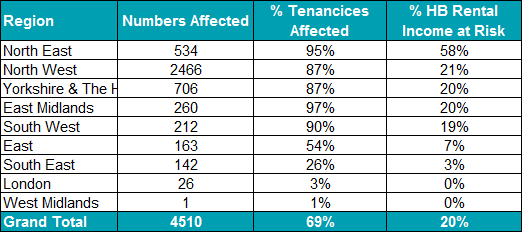

There are also major geographical differences in impact. Table 3 shows a remarkable regional pattern, with the proportion of Riverside tenants’ rental income relying on discretionary local authority top-up ranging from 0% in London (where LHA rates are high, driven by an overheated housing market) and 58% in the North East.

Table 3: Regional impact of LHA caps, Riverside (supported/sheltered)

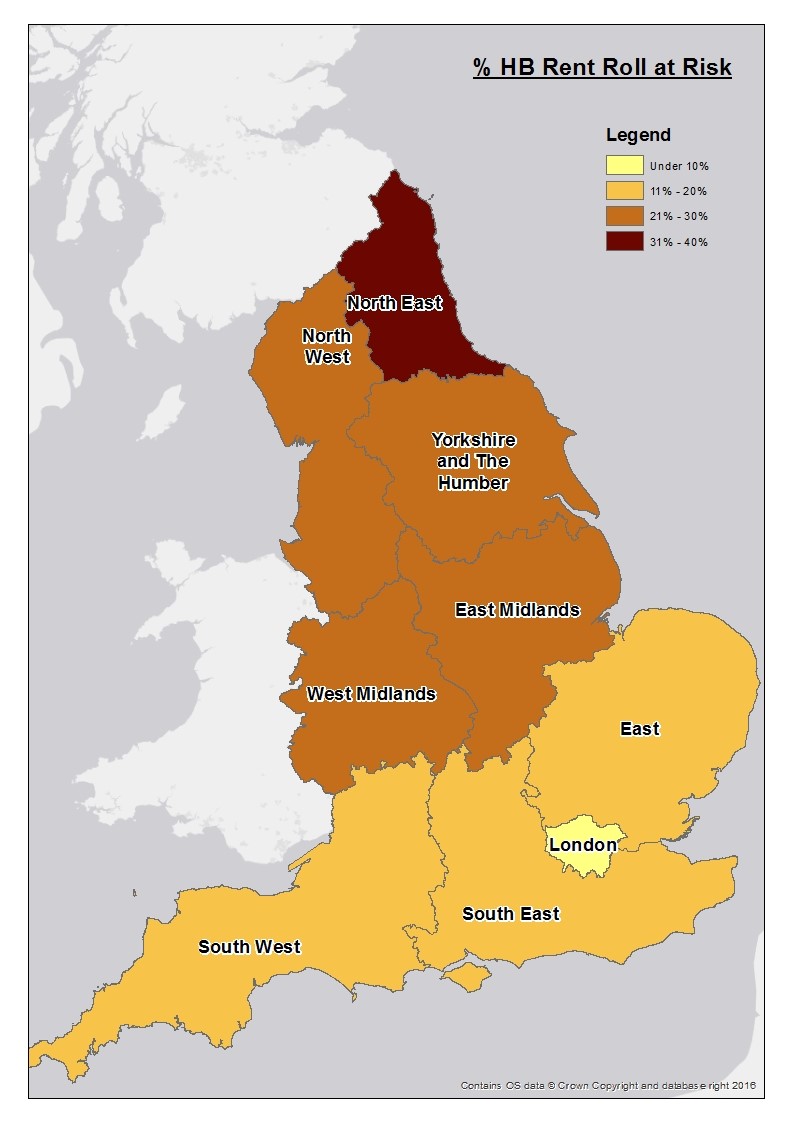

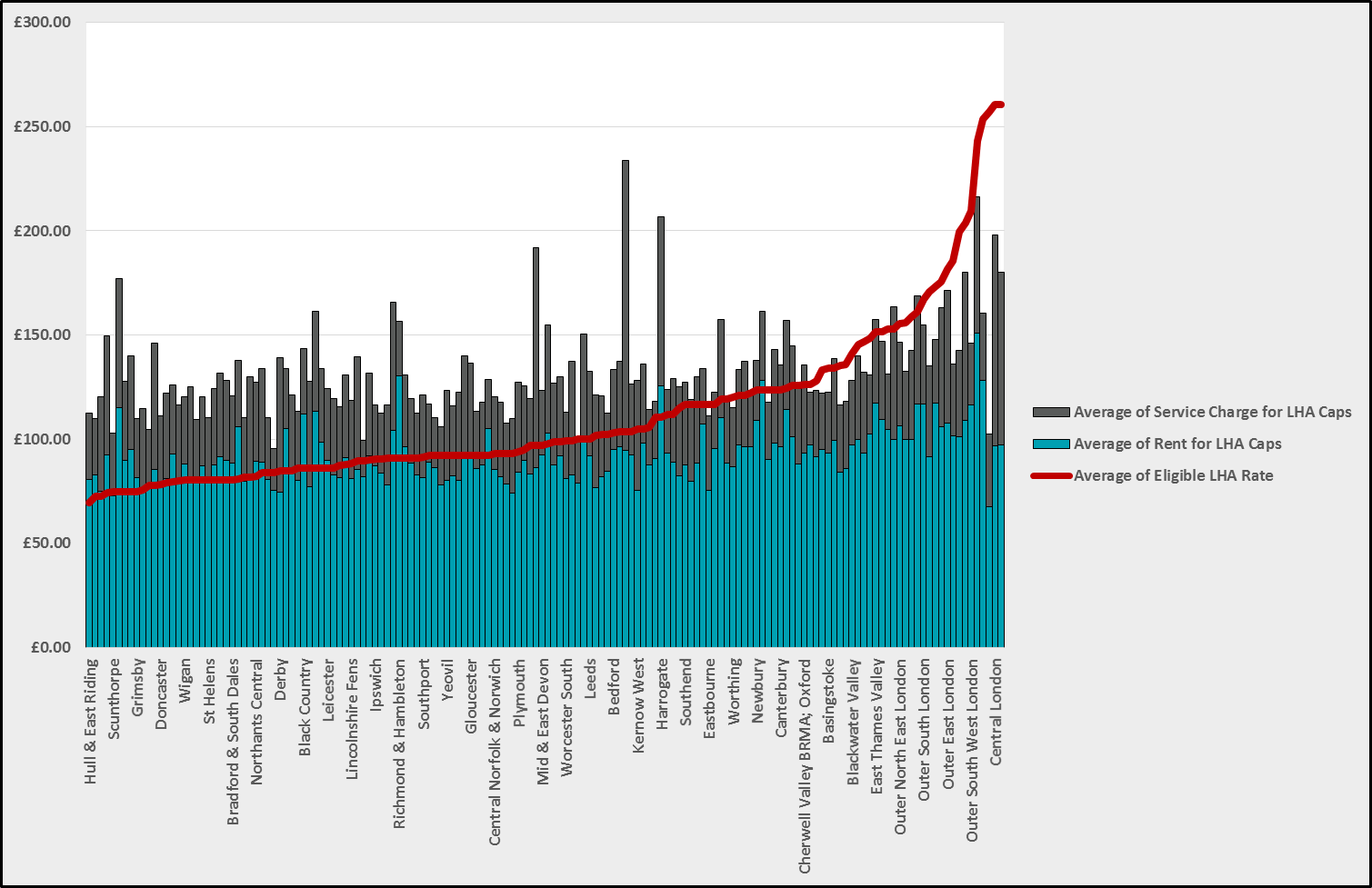

2.6 Again this pattern is repeated using data drawn from the five associations. This is illustrated by the map in appendix 1 showing the percentage of total core rent/service charge income that will be dependent on local top-up funds by English region. This geographical variation is even starker at a local level, and the bar chart in appendix 2 shows average rents and service charges (for the five associations) by BRMA plotted against the one bedroom LHA rate for each area. This illustrates that whilst LHA levels vary from under £70pw in Hull to £260pw in central London, there is no similar variation in sheltered and supported housing rents which are relatively insensitive to location. As a result, the caps hit very hard in the North of England, and much less so, if at all, closer to the capital.

- Answers to consultation questions (selected)

Section IV

Question 8: We are interested in your views on how to strike a balance between local flexibility and provider/developer certainty and simplicity. What features should the funding model have to provide greater certainty to providers and in particular, developers of new supply?

3.1 It is our view that as the proposal currently stands, the Government has struck the wrong balance between local flexibility and provider certainty, with too high a proportion of genuine housing costs moving from entitlement based benefits to local discretionary funding. What is more the extent of this shift varies geographically in a way which unfairly penalises tenants living in lower value areas, meaning that it will be almost impossible for the local top-up funding to deliver its intended outcomes. Our analysis suggests that in Riverside’s case, around twice as much funding is being moved from benefits to local top-up funding than is needed for long-term assurance.

3.2 Because of this, the proposed funding model for supported housing does not provide sufficient certainty to providers and developers who are looking to increase supply. Although the overall level of public funding for supported housing is not currently being reduced, because it is being redistributed from benefits to local funding, the relative security of income fundamentally changes. Where income is underpinned by benefits, which are based on national rules of entitlement which change infrequently and where there is no cash limit, there is a far higher degree of confidence on the part of providers (and their funders) who are tendering for services or planning to invest in new or improved provision, usually relying on thirty year commercial borrowing. Where income depends on locally managed discretionary pots – even if ring-fenced – it is seen as far more vulnerable to cuts and is usually available for planning over a much shorter time frame, typically three years. As paragraph 2.4 illustrates for Riverside, the effect of the LHA caps is that a fifth of funding to meet basic ‘bricks and mortar’ costs is being shunted from benefits to local discretionary funding. This income is therefore seen as less secure and sustainable and doesn’t give providers and their lenders business planning confidence.

3.3 The effects of uncertainty about the future funding model, and now the detailed proposals themselves, have stopped Riverside proceeding with the development of a number of new supported housing schemes which were at a relatively advanced stage. Examples include a scheme for homeless veterans in Colchester, and an extra care scheme in Rochdale. Details are provided in appendix 3 and illustrate very clearly why Riverside’s Board has not been prepared to proceed with this investment, given a complete lack of assurance that basic rent and service charge income will be met through benefits, and the inability of the local authorities concerned to confirm that they will meet additional eligible housing costs (above LHA rates) through the local top-up funds, which of course are yet to be sized or designed.

3.4 This lack of investment confidence in all but the highest value areas is likely to continue, even once local funding arrangements are confirmed. For Riverside, supported and sheltered housing has always been a significant part of Riverside’s development activities, representing 14% of our current 2014-17 programme. However at a time when we are looking to step up our housebuilding programme to respond to the ‘broken’ housing market, supported and sheltered housing are unlikely to play a significant part.

3.5 There are also significant consequences for existing schemes. Riverside is currently completing a 316 unit extra-care scheme in Hull which is PFI funded. The one bed LHA rate in Hull is the lowest in the country at £69.73pw and we estimate that this scheme will require £850,000 each year from the local top-up fund to cover core rent and accommodation-based service charges. With staffing costs, this rises to just over £1m pa. Under the lease, Riverside is obliged to pay a guaranteed amount of rent and service charges based on 95% occupation, and from 2019 our ability to do this will be dependent on the Council’s ability to meet the gap through top-up funding, which it cannot currently commit to. This threatens the long-term viability of a scheme funded through a PFI contract that was entered into in good faith as part of a Government initiative to increase supply, led by Department of Health.

3.6 We believe there is a straightforward way of redressing this balance, and through our modelling we have simulated a range of alternative options to the LHA cap. Our alternative proposals start with LHA as a basis, considering the impact of adding supplements to rates, either at a local, regional or national level.

3.7 Each option has a different impact on sheltered and supported housing, and different geographical regions. Each would increase the security of income for providers and their lenders as it would mean a greater overall proportion of genuine housing costs would be met through the benefits system. Our modelling suggests that the most promising approach would be to apply LHA caps to core rent only, excluding eligible accommodation based service charges which would still be met in full through the benefit system, but driving better value for money through imposing stricter service charge eligibility criteria and fixed tariffs reasonable for different elements of a service charge – e.g. the cost of repairing a lift, maintaining communal gardens etc.

3.8 For Riverside tenants, applying LHA caps to core rents only would practically wipe out any impact on sheltered housing, and reduce the impact on supported housing so that only 10% of total rent and accommodation service charge income is above the cap and therefore ‘at risk’. It practically eliminates any regional variation in all but the lowest value areas.

3.9 Recommendation 1: We propose that using this model (or similar), the sector works with DCLG and DWP through the task and finish groups to devise a suitable proposal which:

- Eliminates the regional inequality of impact of the current proposal, ensuring that the majority of basic rents and accommodation based service charges are met by housing benefit (or UC) where they are eligible, with local top-up funding being used predominantly to meet support costs (principally staffing).

- Lifts the caps above the rent and service charges for sheltered housing, taking the majority of sheltered housing out of the local top-up funding regime. This is particularly appealing given the size of the sheltered housing sector, the relatively small sums by which rent and service charges breach the LHA caps, and the extent of ‘self-payers’ in sheltered housing (27% in the case of Riverside). Removing sheltered housing would result in a major simplification of the local top-up funding system giving local authorities a far better opportunity to make the new system work.

Question 9: Should there be a national statement of expectations or national commissioning framework within which local areas tailor their funding? How should this work with existing commissioning arrangements, for example health and social care, and how would we ensure it was followed?

3.10 Whatever the commissioning arrangement is, it needs to operate within a framework that reflects the fact that local top-up funding will need to meet housing costs (over 50% in the case of Riverside), especially in lower-value areas where LHA rates are depressed. In fact the role of the local top-up fund will vary from area to area – in some areas it will predominantly be funding to compensate for a low-value housing market, in others it will be available to pay for genuine housing support costs, and commissioning new services. Unless this fundamental issue can be addressed through the rebalancing proposed in our answer to question 8, the sizing and design of the top-up funds must reflect this, and a framework established to ensure local funds are applied correctly – this will not be commissioning as local authorities know it!

3.11 Whilst administratively it makes sense for the top-up fund to sit within existing commissioning arrangements – i.e. the upper tier authority where there are two tiers – it is essential that housing professionals from the lower tier or the same authority in unitary areas, are involved in allocating the funds to reflect housing market factors. Within the framework there must be a clear understanding that for most local authorities there will be two different streams within the top-up funds – money for housing support (staff etc.) and money for ‘bricks and mortar’: accommodation-based service charges and in some areas, core rent. When it comes to funding to deliver ‘bricks and mortar’, long-term commitments should be made to provide certainty (10 years plus), and relevant housing related outcomes set, for example around levels of occupancy, maintenance standards etc.

3.12 We welcome a more integrated approach to housing, health and social care, however it is important to recognise that only part of any local ‘top-up’ fund will be available for integration with other funding streams (the support stream). Furthermore, there must be additional funds transferred to local authorities to cover the costs of administration, given that there should be savings in benefit management costs. Previous experience has seen devolved pots eroded by administrative and commissioning costs.

3.13 Where genuine housing support services are being commissioned, any outcomes framework should focus on prevention, acknowledging that supported and sheltered housing services are mainly preventative – for example keeping people out of hospital and social care. This is particularly true of sheltered housing, which provides services to meet lower levels of need, enabling older tenants to retain their independence and providing a secure environment to speed up hospital discharge (see appendix 4 for a case study on added value of housing associations and savings for NHS).[4]

3.14 In terms of outcomes monitoring, local authorities need to recognise that registered providers, including housing associations, are already heavily regulated – this includes rent and service charge setting. Any commissioning and monitoring frameworks must be simple and minimise costs.

3.15 Recommendation 2: Commissioning should sit within a national framework, allowing some local flexibility to meet local circumstances. The national framework should ‘size’ and distribute local pots to reflect local housing markets, ensuring the ring-fence is designed to separate out two funding streams – one to meet ‘bricks and mortar’ costs where LHA rates are low, and another to meet genuine housing support costs. The framework should ensure that local top-up funds are administered by those with the correct expertise (including housing expertise) and that any outcomes and monitoring framework is simple and reflects the preventative nature of much of supported housing.

Question 10: The Government wants a smooth transition to the new funding arrangement on 1 April 2019. What transitional arrangements might be helpful in supporting the transition to the new regime?

3.16 In order to achieve a smooth transition to the new funding arrangement, it is vital that preparation begins as soon as possible. How the local ‘top-up’ fund is both sized and distributed is fundamental to the viability of many supported housing schemes across the country and these decisions must be based on clear local authority led analysis establishing how much top-up is required and what it is needed for, given the scale and cost of existing provision and the level of LHA rates.

3.17 The Government has clearly stated that it values the sector, and so the first priority must be to protect current tenants and existing provision whilst local analysis of need is completed and new administrative arrangement bed in. Funding cannot be cut off at the point of transition on 1st April 2019, and there should be a guarantee of funding at existing levels for all current provision for at least three years, to prepare local authorities for their new role and allow providers to plan ahead. It is only after this that local authorities should be able to re-orientate funding to meet future strategic priorities, whilst taking account of housing market factors.

3.18 The impact of this transition in lower value areas in the north and parts of the Midlands must not be underestimated. The Government must also address how the future of this fund will be managed as LHA rates change after 2020; how local pots will be resized and redistributed must be set out at this early stage.

3.19 Recommendation 3: Preparation on the sizing and distribution of the pot should commence immediately, led by local authorities. Transitional arrangements should be put in place for three years to protect existing provision whilst future strategic priorities are determined.

Question 11: Do you have any other views about how the local top-up model can be designed to ensure it works for tenants, commissioners, providers and developers?

3.20 Given genuine concerns over quality and value for money, it makes sense to design the local commissioning framework to provide better assurance for the tax payer. One simple method would be to restrict access to the local top-up funds (and any enhanced levels of benefit available) to the tenants of registered providers or other landlords in regulated sectors. This would mean that a lighter touch approach to outcome monitoring could be taken.

3.21 It is also crucial that locally devolved funding which is currently paid as housing benefit, does not ‘leak’ to support other local priorities such as adult social care and health. We have already established that the local top-up is primarily housing funding, and the design and longevity of any ring-fencing arrangements need to be watertight. Whilst it is difficult for a Government to make a binding commitment beyond a current Parliamentary cycle, it should use this consultation and the forthcoming Green Paper to secure cross-party consensus on the ring-fenced nature of local top-up funds to ensure they remain in place for as long as possible.

3.22 We are concerned that historically ring-fencing has often proved short-lived due to pressures elsewhere within local authority spending. For example when the ring-fence for Supporting People was removed in 2009, many local authorities stopped funding sheltered housing. Over the past six years Riverside’s income from local authority commissioned services for sheltered housing has fallen by 69% and now stands at an average of £6.77 per week per tenancy. With local authorities under such intense pressure to meet statutory obligations around homelessness and adult social care, there is a strong possibility that top-up funding for sheltered housing would go the same way, making many schemes in their current form unviable.

3.23 Recommendation 4: A watertight ring-fence should be designed to prevent ‘leakage’ of housing funds into other areas of local authority spend. A cross party consensus to retaining the ring-fence beyond the current Parliament should be established.

Section V

Q12. We welcome your views on how emergency and short term accommodation should be defined and how funding should be provided outside Universal Credit. How should funding be provided for tenants in these situations?

3.24 In principle we do not believe that tenants living in short-term, transitional accommodation should be supported in a different way to those living in longer-term supported housing, unless the nature of the accommodation is to provide overnight emergency shelter. In our experience it is very difficult to differentiate between those living in short- and long-term accommodation at the start of the tenancy. Some people living in schemes designed for stays of only a few months end up staying longer. Others moving into longer term accommodation may move far more quickly than expected.

3.25 We believe there is a basic moral principle at stake here – vulnerable people who have the right to occupy their home through a tenancy agreement (no matter for what period) must not lose their entitlement to a universal benefit to meet their housing costs, relying instead on cash limited discretionary funding. Such a system would fail any basic equality impact analysis.

3.26 Once this principle has been established however, there is a perfectly legitimate discussion to be had about the most effective and efficient way of paying benefits, particularly to those whose occupancy may be short-term, given the standard payment cycles associated with Universal Credit.

3.27 One relatively straightforward solution could be an extension of the managed payment system that exists as part of Universal Credit, particularly as administered by landlords enjoying a ‘trusted partner’ relationship with DWP. This permits the delegation of some decision making about the destination and frequency of UC payments to landlords working within a monitored framework.

3.28 Under such an extended arrangement a landlord (normally a registered provider) who is a trusted partner could ‘opt’ to convert the housing cost element of Universal Credit for all tenancies within a scheme into a single block payment, paid directly to the landlord by DWP. In effect the landlord would become a single claimant on behalf of all tenants living in an entire scheme, who would be ‘passported’ to a direct payment, paid as part of the block. Within such a framework, DWP could make a single monthly payment to the ‘trusted’ landlord based upon assumptions about occupancy levels and tenant eligibility. The landlord would be expected to retain accurate monitoring information which could be audited, allowing an annual reconciliation of block grant paid to entitlement based on occupancy and eligibility. In this way the bulk of the administrative burden and risk would lie with the landlord rather than DWP.

3.29 This arrangement would only be open to certain categories of supported housing schemes, and to those landlords who could meet the quality threshold required of a trusted partner. Indeed where the circumstances of a scheme or service suit, there could still be an option for those providers who wish to work with tenants to apply for Universal Credit individually to do so, for example to promote independence and to prepare tenants for moving on to mainstream accommodation.

3.30 Depending on the level of LHA caps, the landlord may still depend upon locally administered top-up funding to meet housing support costs, and this would work in exactly the same way as it would for longer-term forms of supported and sheltered housing.

3.31 Recommendation: for short-term and transitional accommodation which is subject to tenancies, support for housing costs should be met through the benefits system, with regulated landlords able to ‘opt’ to convert individual payments into block payments, within a ‘trusted partner’ framework which places a responsibility on the landlord to track and reconcile eligibility and vacancies.

Appendix 1: Impact of LHA caps by English Region, 5 associations

Appendix 2: Average rent/service charges by BRMA, and I bed LHA rate – five associations [5]

Appendix 3: Examples of Stalled schemes

Keswick Close Extra Care – Rochdale

Keswick Close is a planned extra care scheme in Middleton, Rochdale. It will comprise 98 homes, a mix of one and two bedroom apartments and bungalows. The majority of homes are for rent, although the scheme includes 11 for shared ownership and 7 for outright sale. The scheme is being supported by £3m of public investment through the HCA.

Keswick Close is currently ‘on hold’ as a result of revenue funding uncertainty related to the proposed introduction of LHA caps to housing benefit, given that the majority of tenants are likely to be benefit dependent in this low income areas. The imposition of caps will mean that tenants will face a shortfall in housing benefit representing over 25% of rent and service charges in the case of a 1 bed flat and 18% in the case of a two bed as illustrated below.

|

Scheme details |

LHA weekly cap |

Proposed Target Rent Riverside + service charge |

Shortfall of approx. per week |

|

1 bed flat |

£101.98 |

£82.56 + £54.00 |

£34.58 |

|

2 bed flat |

£119.98 |

£92.96 + £54.00 |

£26.98 |

Without additional funding, it is highly unlikely that tenants would be able to make up this level of shortfall from their own incomes, and so the scheme would simply not be viable. The availability of local top-up funding has not been confirmed. Local residential care costs range between £400 and £1000 per week, depending on the extent of need related to conditions such as dementia. In this context, our proposed scheme offers excellent value for money.

Colchester Homeless Veterans Scheme

This scheme comprises 50 units of supported housing for homeless veterans: 30 x 1 bed flats receiving high levels of support and 20 x 1 bed flats offering a move-on facility.

We have received a £4.5m capital allocation from the Veterans Accommodation Fund administered by MoD. The scheme has also received internal approval for significant additional subsidy from Riverside.

This scheme is currently ‘on hold’ as a result of uncertainty over revenue funding and we have requested confirmation from Essex County Council of their long-term commitment to ‘top-up’ funding for this development. However despite council support for the scheme, they are not in a position to commit to funding the gap at present.

The table below shows the current projected impact of the LHA cap for each tenant.

|

Scheme details |

LHA weekly cap |

Proposed Target Rent + service charge |

Shortfall of approx. per week |

|

1 bed flat |

£103.56 |

£136.33 + £24.50 |

£57.27 |

|

1 bed flat |

£103.56 |

£136.33 + £14.00 |

£46.77 |

The total annualised shortfall in rent in the first year of operation would be £137,982 representing 34% of total rental and accommodation based service charge income. Core rents alone are higher than LHA caps by more than £30 per week.

Appendix 4: Case Study – SB (initials changed to protect privacy)

In August 2016, The Boundaries received an email from the local health authority requesting us to assess a patient that had been admitted in Queen’s Hospital, Romford for three to four months. SB, a 24 year old man, had spent some time in intensive care due to complications from poor management of diabetes. Once SB was stabilised he should have been discharged back to his Private Sector Leasing (PSL) flat in the community. However the consultant in charge of his physical wellbeing at Queen’s Hospital recognised the complex nature of SB’s case – namely that his mental health issues were seriously impacting on his physical health in a life-threatening way. It was also recognised that physically he would not be able to manage in his third floor flat and so SB became a Delayed Transfer of Care (DTOC) patient at Queen’s Hospital. With current estimates by London Trust standing at £800 for an overnight stay on a ward, North East London Foundation Trust desperately needed to find community support for SB, not only due to costs but also for his needs. When we were asked to carry out an emergency assessment SB’s discharge from the ward had already been delayed by five weeks.

SB needed a supported placement for a period of assessment from Havering’s brief intervention mental health team (HAABIT) as there were some doubts about the level of his engagement with services and the suitability of his current home. The Boundaries has an assessment room for just this purpose but it was already in use. It became clear that we needed to work flexibly with Havering’s Social Care Lead in order to support this assessment period and ensure that SB’s support needs were met. We made an offer of a recently vacated room, usually funded through housing benefit, for this period. It was agreed that the discharge team at North East London Foundation Trust would cover the costs of both rent and support charges during this time and SB would have a short licence to cover this period. The cost of this was £338 per week including rent, service charges and support cost (which are typically the responsibility of the customer) plus the regular commissioned £405 support cost. This totalled a cost to the Trust of £743 per week as opposed to the estimated weekly cost of a ward admission of £5,600 per week.

SB’s assessment lasted for a period of three months with an outcome that his needs were assessed as too high to return to his PSL flat. He was then offered a longer-term placement at The Boundaries.

Over both the assessment period and as part of his ongoing support we have been able to support SB to avoid further hospital admissions, which HAABIT have judged would have been unavoidable if he had returned home. SB has also engaged well with his multidisciplinary team and, at a recent Professionals Meeting, the social worker assessing him was forthright in her opinion that if we had not all been able to work together to achieve this level of support for SB then it is very likely that he would be a statistic by now.

SB was also a frequent attender to both A&E departments and his GP due to the complexity of his physical and mental health needs. Since receiving 24 hour support at The Boundaries over the last four months he has not visited either service. It is difficult to estimate the cost savings to the Trust due to this but there is no doubt that there is one.

SB now has structured appointments with his Diabetic Nurse and GP. He is engaging well, attending intensive therapy with IMPART, and managing his medication independently and much more effectively than when he was living alone. We see observable improvements in his health week by week and SB now speaks in terms of aspirations rather than self-harm and hopelessness. The added value of support housing cannot be underestimated.

[1] Throughout this document we tend to use the terminology “supported” and “sheltered” housing, the latter referring to specialist housing for the elderly with some limited communal facilities and services.

[2] In undertaking this exercise, we have already assumed that for supported housing (but not sheltered), staff based service charges will not be met by housing benefit/Universal Credit, but that this element of our costs will rely on local top-up funding.

[3] Riverside, St Mungos, Housing and Care 21, Hanover, Home Group – with the support of Homeless Link and Lord Best. Together we own 46,000 sheltered and supported housing units, c 11% of English stock. Whilst not claiming to be representative, we believe we are ‘typical’ of the sector.

[4] For an overview of the preventative value of sheltered and extra care housing see ‘The Value of Sheltered Housing’, James Berrington for NHF, January 2017.

[5] Data for all BRMAs shown but not listed due to space constraints – version with full list available on request